Mortgage Investment Corporation Things To Know Before You Buy

Mortgage Investment Corporation Things To Know Before You Buy

Blog Article

An Unbiased View of Mortgage Investment Corporation

Table of ContentsThe Ultimate Guide To Mortgage Investment CorporationThe smart Trick of Mortgage Investment Corporation That Nobody is Talking AboutMore About Mortgage Investment CorporationExamine This Report on Mortgage Investment CorporationGetting My Mortgage Investment Corporation To WorkIndicators on Mortgage Investment Corporation You Should Know

After the lending institution sells the financing to a home mortgage capitalist, the lending institution can make use of the funds it gets to make even more car loans. Giving the funds for lending institutions to produce more fundings, financiers are essential because they establish standards that play a function in what types of loans you can obtain.

Department of Veterans Affairs sets standards for VA loans. The U.S. Department of Farming (USDA) establishes standards for USDA lendings. The Government National Home Mortgage Association, or Ginnie Mae, manages government mortgage programs and insures government-backed financings, securing private capitalists in situation borrowers default on their financings. Jumbo lendings are home mortgages that exceed adapting car loan limits. Since there is more danger with a larger home loan quantity, jumbo finances tend to have more stringent borrower qualification requirements. Financiers additionally handle them in different ways. Traditional big car loans are generally as well large to be backed by Fannie Mae or Freddie Mac. Instead, they're marketed directly from lending institutions to private financiers, without involving a government-sponsored venture.

These companies will certainly package the lendings and offer them to exclusive capitalists on the secondary market. After you close the finance, your lender may sell your funding to a capitalist, yet this usually does not transform anything for you. You would certainly still make payments to the loan provider, or to the home loan servicer that manages your home mortgage settlements.

Mortgage Investment Corporation Can Be Fun For Everyone

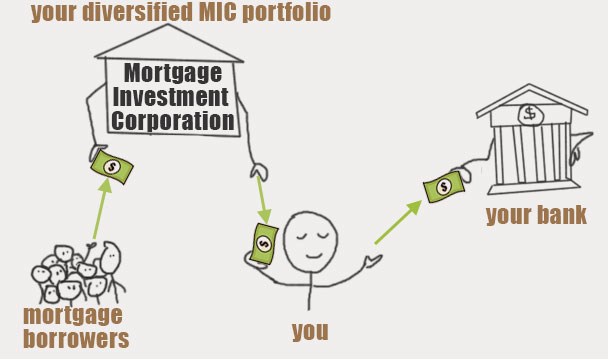

How MICs Source and Adjudicate Loans and What Takes place When There Is a Default Home mortgage Financial investment Companies offer investors with straight exposure to the property market with a pool of thoroughly selected mortgages. A MIC is accountable for all aspects of the home loan spending process, from origination to adjudication, consisting of everyday monitoring.

CMI MIC Finances' rigorous credentials process enables us to take care of home loan quality at the really onset of the financial investment process, reducing the possibility for payment issues within the lending profile over the term of each mortgage. Still, returned and late settlements can not be proactively handled 100 percent of the time.

We buy home mortgage markets across the nation, enabling us to lend throughout copyright. To get more information regarding our investment procedure, get in touch with us today. Contact us by filling in the type listed below to find out more concerning our MIC funds.

How Mortgage Investment Corporation can Save You Time, Stress, and Money.

A MIC is additionally thought about a flow-through financial investment lorry, which means it should pass 100% of its annual take-home pay to the shareholders. The returns are paid to investors frequently, typically each month or quarter. The Revenue Tax Obligation Act (Section 130.1) details the requirements that a company have to satisfy to qualify as a MIC: A minimum of 20 shareholdersA minimum of 50% of assets are property mortgages and/or money deposits guaranteed by the copyright Down Payment Insurance Policy Firm (CDIC)Less than 25% of funding for every shareholderMaximum 25% of resources invested into real estateCannot be associated with constructionDistributions filed under T5 tax obligation formsOnly Canadian home mortgages are eligible100% of net income goes to shareholdersAnnual monetary statements audited by an independent bookkeeping firm The Home loan Investment Corporation (MIC) is a specialized economic entity that spends mostly in mortgage.

At Amur Resources, we intend to give a genuinely varied method to alternate investments that make the most of yield and capital conservation. By offering a series of traditional, earnings, and high-yield funds, we satisfy a series of spending objectives and choices that fit the needs of every specific investor. By purchasing and holding shares in the MIC, shareholders gain a symmetrical ownership passion in the business and receive earnings through reward payouts.

On top of that, 100% of the financier's capital gets placed in the chosen MIC with no in advance transaction charges or trailer YOURURL.com fees. Amur Funding is concentrated on supplying investors at any type of degree with access to professionally took care of private financial investment funds. Investment in our fund offerings is readily available to Alberta, British Columbia, Manitoba, Nova Scotia, and Saskatchewan citizens and should be made on an exclusive placement basis.

Purchasing MICs is a wonderful method to gain direct exposure to copyright's growing genuine estate market without the demands of energetic residential property management. Apart from this, there are a number of various other reasons that financiers take into consideration MICs in copyright: For those seeking returns comparable to the securities market without the associated volatility, MICs supply a protected realty investment that's easier and might be a lot more rewarding.

Mortgage Investment Corporation Fundamentals Explained

Actually, our MIC funds have actually traditionally provided 6%-14% annual returns. * MIC capitalists obtain rewards from the passion settlements made by debtors to the home mortgage loan provider, developing a constant passive income stream at higher prices than standard fixed-income protections like federal government bonds and GICs. They can additionally pick to reinvest the rewards into the fund for compounded returns

MICs presently make up roughly 1% of the overall Canadian home mortgage market and stand for a growing segment of non-bank economic business. As investor need for MICs grows, it is necessary to recognize exactly how they work and what makes them various from standard property financial investments. MICs buy mortgages, unreal estate, and as a result offer direct exposure to the housing market without the added danger of building possession or title transfer.

typically between 6 and 24 months). Mortgage Investment Corporation. In return, the MIC accumulates rate of interest and fees from the borrowers, which are after that distributed to the fund's preferred investors as returns payments, generally on a regular monthly basis. Because MICs are not bound by much of the very same strict lending demands as conventional financial institutions, they can establish their very own requirements for accepting loans

Mortgage Investment Corporation Fundamentals Explained

This indicates they can bill higher passion rates on home loans than traditional banks. Home mortgage Investment Companies additionally delight in special tax obligation treatment under the Earnings Tax Obligation Work As a "flow-through" investment automobile. To avoid paying revenue tax obligations, a MIC needs to disperse 100% of its internet income to investors. The fund has to have at least 20 shareholders, without investors owning even more than 25% of the outstanding shares.

Situation in factor: The S&P 500's REIT group vastly underperformed the wider stock market over the past five years. The iShares united state Realty exchange-traded fund is up much less than 7% given that 2018. By contrast, CMI MIC Finances have actually historically produced anywhere from 6% to 11% annual blog here returns, depending on the fund.

In the her comment is here years where bond yields constantly declined, Mortgage Financial investment Firms and other alternate assets grew in appeal. Returns have rebounded since 2021 as reserve banks have actually increased rates of interest yet genuine yields remain negative about rising cost of living. Comparative, the CMI MIC Balanced Mortgage Fund created an internet yearly yield of 8.57% in 2022, like its efficiency in 2021 (8.39%) and 2020 (8.43%).

Not known Details About Mortgage Investment Corporation

That is why we want to aid you make an educated choice regarding whether or not. There are numerous advantages connected with buying MICs, including: Since financiers' money is merged together and spent across numerous residential or commercial properties, their portfolios are branched out across various real estate kinds and debtors. By owning a portfolio of home mortgages, financiers can alleviate risk and stay clear of putting all their eggs in one basket.

Report this page